If your insurer has flagged your Poly B plumbing, sent a non-renewal notice, or applied a surcharge to your last renewal, you are not dealing with an edge case. This is now standard policy across the majority of Canadian insurance carriers — and it is accelerating. Homes in Calgary and throughout Alberta that were built between 1985 and 1998 are the primary target because that is the window when polybutylene pipe was most heavily installed across Western Canada.

This page explains exactly what insurers are doing, why they are doing it, what the consequences are if you ignore a notice, and what it takes to get your coverage reinstated or preserved.

Why Insurers Are Treating Poly B as an Uninsurable Risk

Insurance underwriters make decisions based on actuarial data — the statistical likelihood of a claim. Poly B pipe has an established and well-documented failure pattern that insurers have been tracking for decades. The pipe degrades from the inside out, developing micro-fractures along its walls and at the acetal fittings that connect segments. These fractures are not visible from the outside. They develop silently, and when they fail, they typically fail behind drywall — which means water runs freely before anyone notices.

The chemical driver in Alberta is chloramine. Calgary and Edmonton both treat municipal water with chloramine as a disinfectant, and chloramine is more persistent and chemically aggressive than the standard chlorine used in other regions. Poly B systems in Alberta are reaching failure faster than the same pipe installed in other provinces. Insurers underwriting Alberta properties know this and have priced it into their risk models.

Water damage is already the single most expensive claim category in Canadian home insurance. The average Poly B-related water damage event — a fitting failure behind a wall — runs between fifteen thousand and forty thousand dollars in remediation costs depending on how long the water ran before detection. When that risk is attached to a specific, identifiable pipe material with a known failure timeline, insurers stop treating it as a random event and start treating it as a scheduled liability. At that point, coverage becomes conditional or unavailable.

Four Ways Alberta Insurers Are Responding to Poly B

Not every insurer handles Poly B the same way. Understanding which response you are dealing with determines how urgently you need to act and what your options are.

- Premium surcharge with continued coverage. The insurer identifies Poly B during a renewal assessment and adds a flat-dollar or percentage surcharge to reflect the elevated risk. Coverage continues but at a higher annual cost. This is increasingly uncommon as carriers move to harder positions.

- Water damage exclusion rider. The carrier renews the policy but excludes water damage caused by plumbing failure. This is a particularly dangerous outcome because most homeowners do not fully register what this exclusion means until they file a claim and have it denied. The policy looks intact. The most likely claim category is not covered.

- Conditional renewal with a remediation deadline. The insurer issues a renewal notice with a condition: Poly B must be replaced by a specified date and documented confirmation must be provided, or coverage will not continue. This is now the most common response from major Alberta carriers and gives homeowners a fixed window to act.

- Non-renewal or cancellation. The carrier declines to renew the policy at the end of its term or, in some cases, cancels mid-term. Coverage terminates on a specific date. Finding a replacement policy on a home with confirmed Poly B, on short notice, is difficult and expensive.

The Carriers Calgary Homeowners Are Hearing From

The shift in underwriting policy is industry-wide, but three carriers have been consistently named by Calgary homeowners receiving non-renewal or conditional renewal notices: Intact Insurance, Wawanesa Mutual, and Economical Insurance. These are not fringe providers — they are among the largest home insurance carriers in Alberta, which means a significant portion of Calgary homeowners with Poly B are receiving these notices directly from their current insurer rather than finding out about the policy shift when they shop for a new one.

Homeowners who receive notices from these carriers have a narrow window. Conditional renewal deadlines are typically sixty to ninety days from the notice date. Non-renewal notices follow the same general timeline — coverage ends at the policy renewal date, and if no compliant replacement insurer has been secured by then, there is a coverage gap.

What a Coverage Lapse Actually Costs You

A gap in home insurance coverage is not just an inconvenience. For most Calgary homeowners with a mortgage, it creates an immediate problem with the lender. Mortgage agreements in Canada require continuous property insurance as a condition of the loan. If coverage lapses, the mortgage lender has the right to force-place insurance on the property — an insurer selected by the bank, not by you, at a premium that is typically two to four times what standard coverage costs. The lender invoices you for that cost directly.

Beyond the mortgage problem, a coverage gap means any event that occurs during the lapse period — fire, hail, break-in, water damage from any source — is entirely your financial exposure. A single pipe failure in a home with no active insurance policy can result in a five-figure remediation bill with no coverage to offset it.

Homeowners who receive a conditional renewal notice and do not act within the deadline often discover, too late, that finding a new carrier willing to issue a new policy on a home with unresolved Poly B is significantly harder than renewing with their existing insurer under the conditional terms they rejected.

What Documentation Insurers Require to Reinstate Coverage

An insurer cannot reinstate or confirm coverage based on a homeowner’s verbal assurance that the work is done. What closes an insurance file is a specific documentation package from the contractor who completed the work. That package typically needs to include:

- Written confirmation of the scope of work completed, including confirmation that the full Poly B system was removed

- Specification of the replacement material installed (PEX — cross-linked polyethylene — is the standard accepted replacement)

- Certification that the tradespeople who performed the work hold a Red Seal journeyman plumbing certification

- A pressure test result confirming the integrity of the new system at installation

- The contractor’s business information, licence number, and contact details

Insurers vary in exactly how they want this documentation formatted, but every carrier that conditions coverage on Poly B removal requires some version of this package before they act on the file. Homeowners who use contractors who do not provide completion documentation in this form create a secondary problem on top of the replacement cost — their insurer may not accept the work as satisfactory remediation even after the job is physically complete.

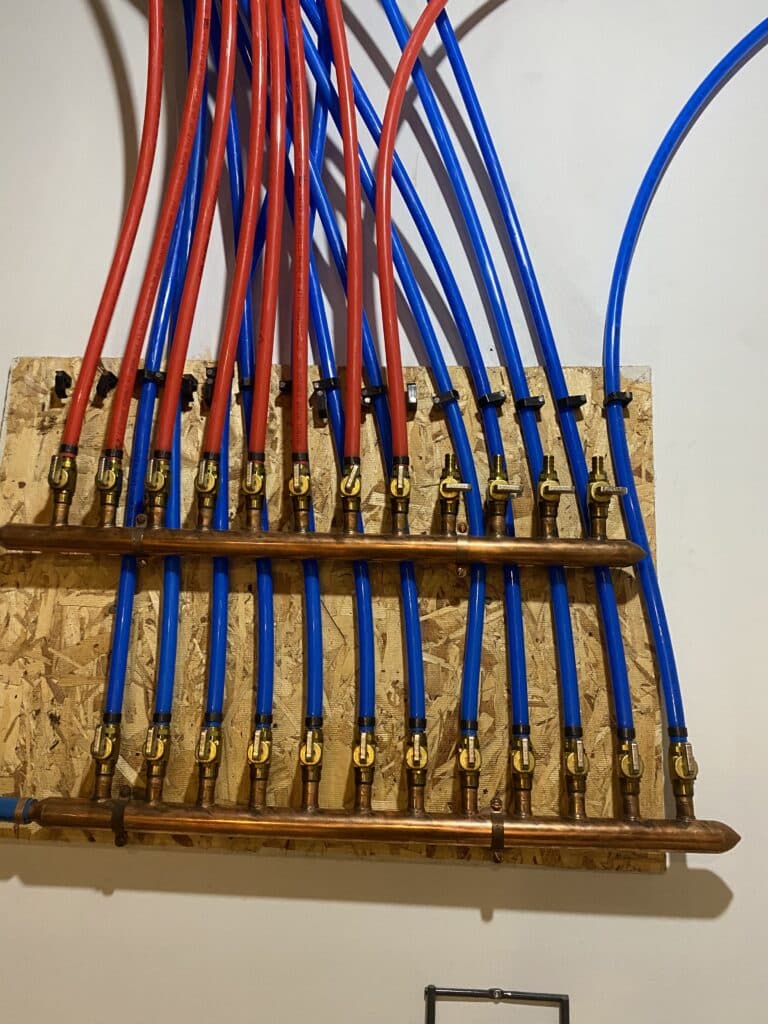

How Full Replacement Resolves the Insurance Problem

The only remediation that satisfies insurance underwriters across the board is complete removal of the existing Poly B system and replacement with PEX piping throughout the home. Partial replacement — replacing only the accessible sections or the sections that have already failed — does not resolve the underwriting concern because the remaining pipe has aged at the same rate and carries the same failure risk. Insurers are aware of this approach and most explicitly reject partial remediation as sufficient for coverage reinstatement.

A full replacement job that is properly documented does reliably resolve the insurance problem. Once the completion documentation is submitted, most Alberta carriers confirm reinstated or unconditional coverage within thirty to sixty days. Homeowners who front-load the replacement — booking a contractor before engaging their insurer about reinstatement — are in a significantly better position than those who wait for the insurer to confirm what they need before starting.

What to Look for in a Replacement Contractor

The quality of the replacement job and the quality of the documentation it generates are directly connected to the contractor you choose. A general plumbing company taking on a Poly B replacement as one project among many will not necessarily understand what an insurance underwriter needs from the completion package, and may not have a structured process for producing it.

The Poly B Plumbing Guys operates across Calgary and Western Canada as a contractor that works exclusively on polybutylene removal and PEX installation. Because insurance-driven Poly B replacement is the core of the business, the scoping, scheduling, and documentation process is built around producing exactly what insurers need to act on a file. The company’s Red Seal certified tradespeople work on a fixed-price contract model — the quoted price does not move regardless of what is found behind the walls — which eliminates cost uncertainty on a job that is already being done under deadline pressure.

Before booking any contractor, confirm three things: that the scope includes removal, PEX installation, and full drywall restoration under one contract; that the price is fixed; and that the completion documentation they provide will satisfy your specific insurer’s requirements. If a contractor cannot answer all three questions clearly, keep looking.

Getting Ahead of the Problem

Calgary homeowners who have received a notice and have fewer than ninety days left have a workable path to reinstatement — but the time required to get a scope, sign a contract, complete the job, and submit documentation to the insurer means there is no room to wait. Every week of delay compresses the window between job completion and the coverage deadline.

Homeowners who have not yet received a notice but know their home was built between 1985 and 1998 are in a better position than those responding to a notice — but the trajectory of carrier underwriting policy is clear. The number of Alberta insurers who will continue to cover Poly B homes without condition is declining each renewal cycle. Acting before a notice arrives means acting on your own timeline, not your insurer’s.

A full scope and fixed-price quote from The Poly B Plumbing Guys is the fastest way to understand exactly what replacement involves for your Calgary home — and to have a number and a timeline in hand before your next conversation with your insurer.